Of all the elements that lead to an approved mortgage loan, your credit report is the most important, and often misunderstood, part of the process.

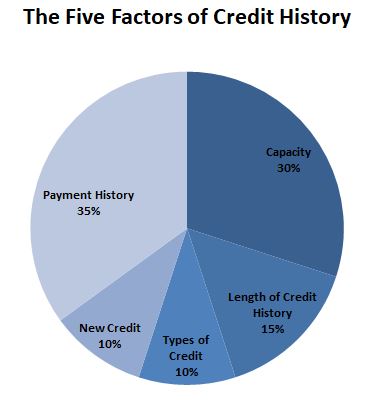

Unlike down-payment money and your employment/income, which represent your current financial position, your credit history represents your financial behavior throughout your adult life. This is a much more complex situation and it’s hard to “fix” any problems overnight. Traditionally, the best indication of a person’s future financial habits is their past financial habits, so lenders use past credit data to help assess the risk of the borrower defaulting or paying late on the loan.

There are a wide variety of things you can do to both improve credit “dings” on your report and avoid decisions that could lead to a drop in your FICO® score. Here are some of the most importing things you can do, or not do, to help make your credit score as favorable as possible:

DO NOT apply for new credit cards or car loans during the 12 months preceding your mortgage application.

DO keep all your credit card balances between 25% and 50% of their available credit limit. Maxing out your credit cards can reduce your FICO® score by as much as 60 points, even if you’re paying on time!

DO NOT close old accounts. A lengthy credit history helps to establish a higher credit score, so closing old account can actually lower your FICO® score.

DO avoid paying your bills after the 30 day late deadline. Even one late payment can drop your FICO® score by as much as 100 points! Late payments or open collections accounts, impact your credit score the most if they are 1 to 12 months old. The impact decreases if they are between 13 to 24 months old and decrease even further after they are 2 years old.

DO NOT pay off collections that are over 2 years old. Doing so will lower your FICO score. If the collection is less than 2 years old, pay it off if possible.

Ready to start the mortgage loan process or have a question that isn’t answered here? Contact us today!